Housing and Mortgages

The following post compiles what I’ve learned in Module 3 of the course.

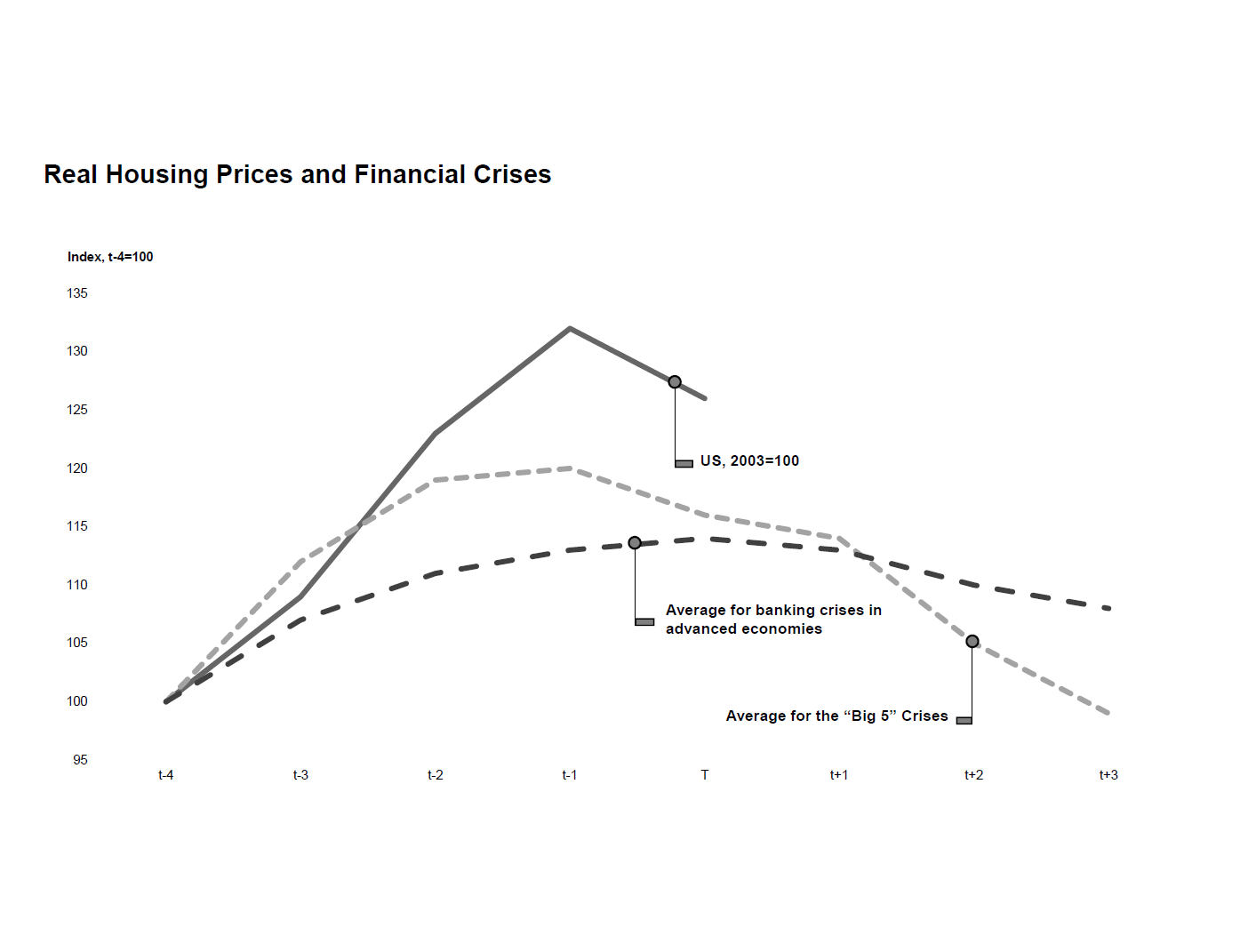

Reinhart and Rogoff studied the big 5 crises and other 13 bank-centered crises and noted that housing appreciation is general feature of financial crises.

To understand the financial crisis, we first need to understand the housing crisis and for that we need to know about mortgages.

Yes, The Financial crisis and the Housing crisis are different, The Housing crisis was a primary driver for The Financial crisis which then led to The Great Recession.

Mortgages

Fixed: The standard mortgage in the United States has a 30-year term, with fixed interest rates. Every year you pay interest and an amortization of the loan.

Adjustable: These have adjustable interest rates for all or part of the term (“ARMs”, 2/28, 5/25 or 5/1) with the adjustable rate set to some spread above a reference rate. Initial fixed rate will typically be lower than for 30-year fixed mortgage, sometimes called a teaser.

Mortgages can also divided as below

Prime: These mortgages conform with the measures set by the government on various parameters. These then can be packed and sold as Mortgage backed securities to Government Sponsored Enterpises which are then insured by them.

NonPrime: Subprime: Targetted to those who have tarnished credit histories and have little savings for down payments.

Alt-A: These are near prime mortgages given to those who have minor problems in credit.

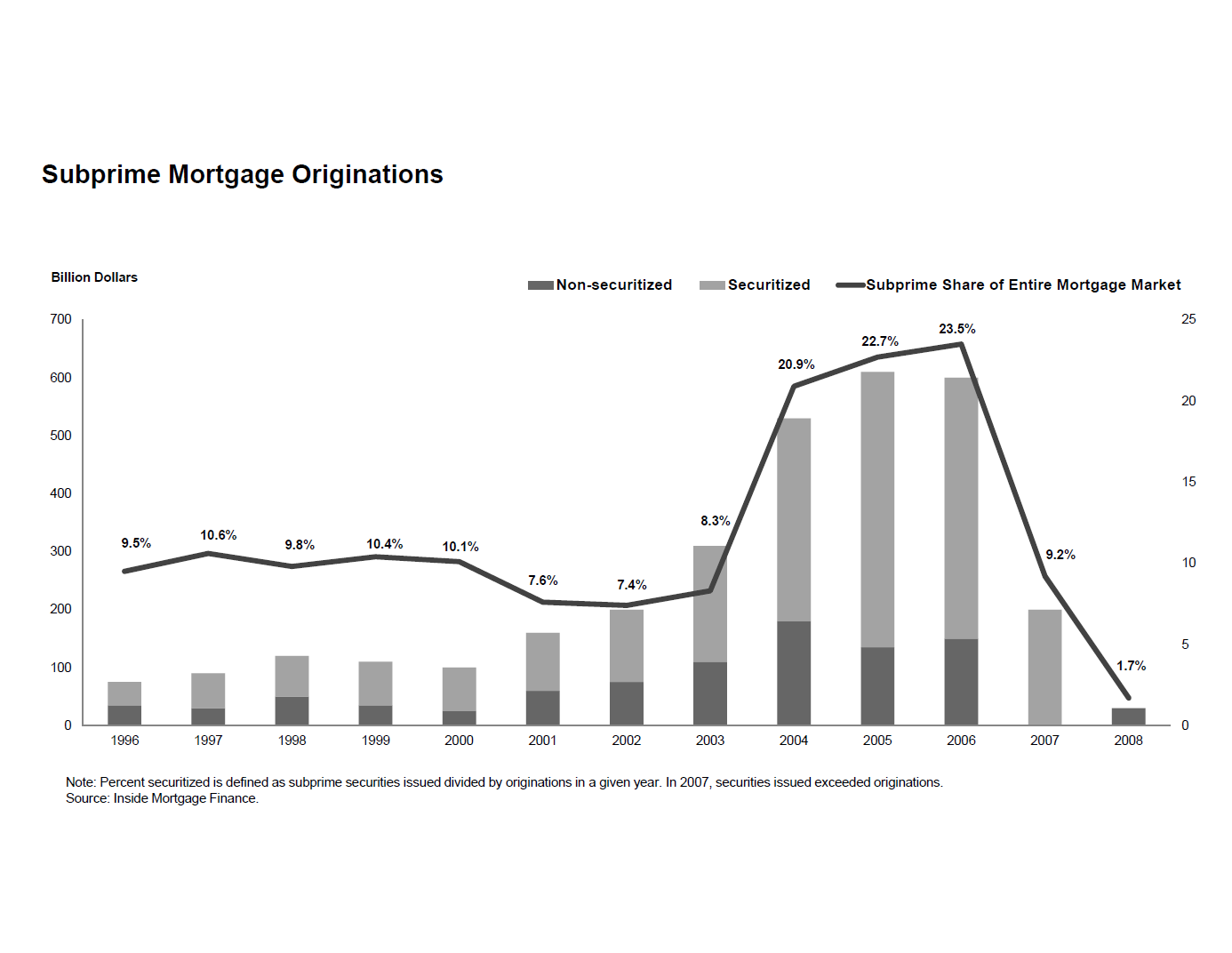

In 2000s, Subprime Mortgages exploded.

Note: Observe that a major chunk of Subprime loans were securitized. We’ll use that in a later module.

Subprime Mortgages - Are they designed to fail?

In a typical subprime mortgage, an initial “teaser” rate will be set to adjust relative to a short term interest rate, say the libor rate after two or three years, usually to be much higher than the original rate.

A borrower can get out of this higher rate by refinancing, but this action may incur a pre-payment penalty.

This sounds like a horrible trap, like a financial product that is “designed to fail”.

So when will these subprime mortgages make sense?

-> When everybody expects housing prices to increase. Let’s see how that’ll work.

Let’s say the home value at time t is 100,000 dollars and initial “equity” (down payment) in the house is 10,000 dollars. Now the home appreciates to 120,000 dollars after 3 years. The owner’s equity rises to 30,000 dollars! So the owner will refinance his loan after 3 years from a new bank which will give them a slightly bigger mortgage due to appreciation of the house and they will incur a pre-payment penalty from the old bank and pay them off using the slighty bigger mortgage from the new bank and this way no extra money goes out of their pocket and they have more equity in the house!

That might not be clear at first, go ahead read it multiple times, it’s not like you have some deadlines. (That’s why you are still reading this stupid blog right?)

Foreclosure

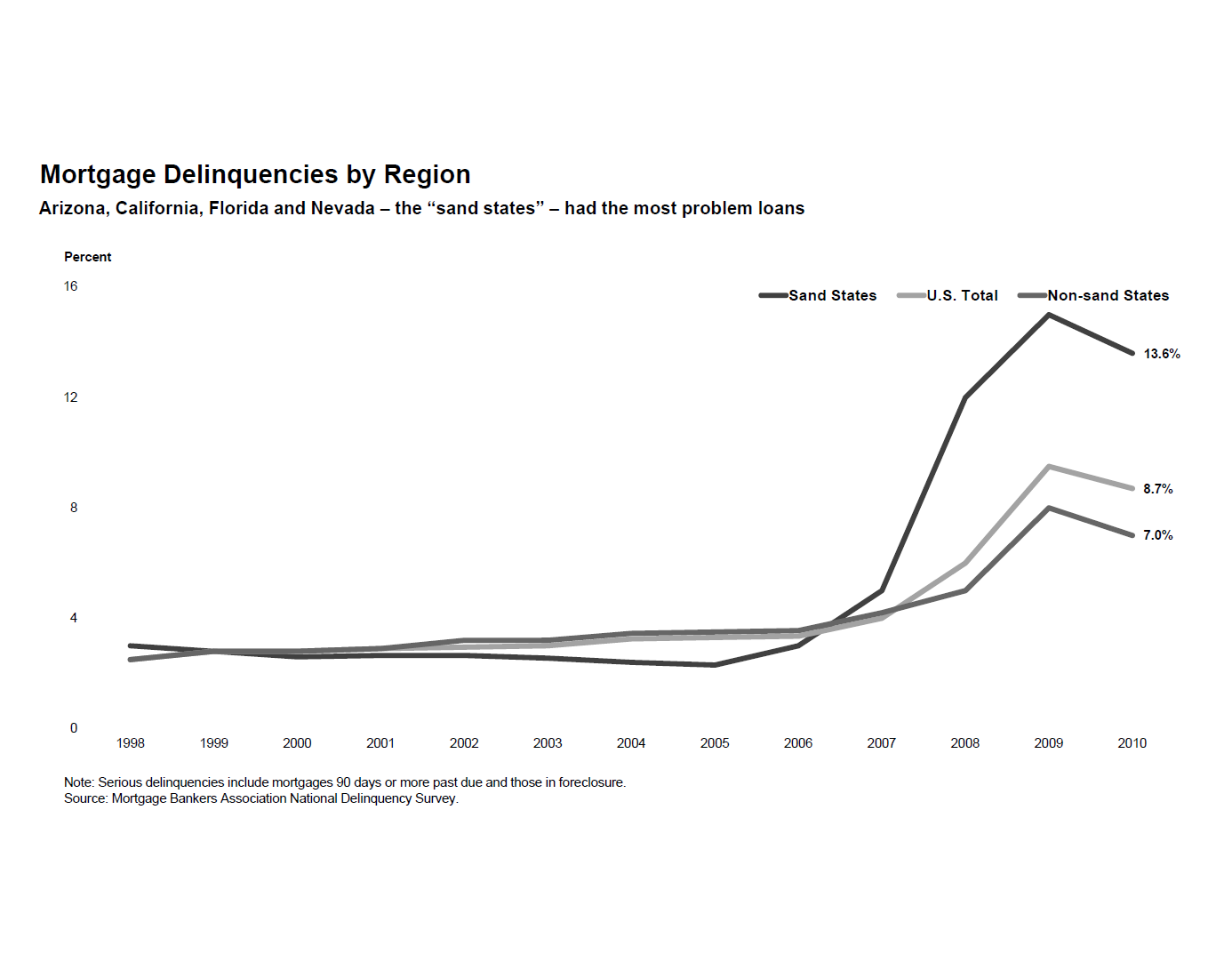

In the United States, foreclosure was a national phenomenon, but was worst in the sand states of: Arizona, California, Florida, Nevada. (Where you get to see them beaches)

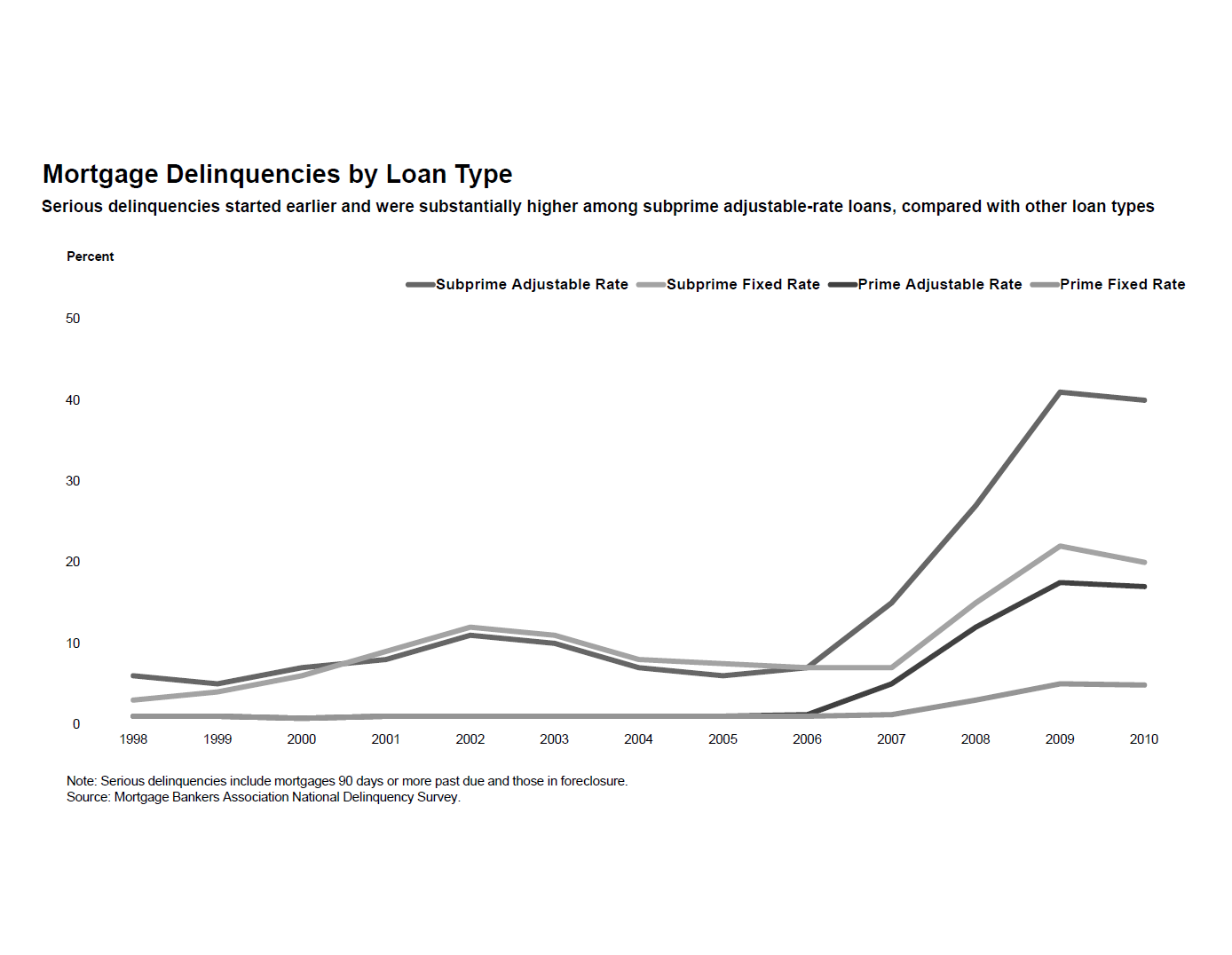

All types of loans had a high foreclosure rate with the subprime adjustable loans performing the worst.